by Suman Gupta

Mumbai, July 10, 2025: — Emkay Global Financial Services, in its latest BFSI-Banks report highlighted a muted Q1FY26 earnings season for private sector banks (PVBs), largely due to sluggish credit growth and a sharp contraction in margins following aggressive repo rate cuts. In contrast, public sector banks (PSBs) are likely to demonstrate stronger earnings resilience, supported by relatively milder margin compression and higher treasury gains.

The report highlights that system-wide credit growth remained modest at ~10% YoY, while deposit growth was slightly better at ~11% YoY. This weak momentum, coupled with recent lending rate reductions, has resulted in 5–20bps QoQ margin compression across the board—with large PVBs bearing the brunt.

While most private banks are likely to report muted profitability—with Axis Bank and IndusInd Bank impacted by weak margins and elevated credit costs—Emkay identifies ICICI Bank, Indian Bank, SBI, and KVB as positive outliers. Meanwhile, SBI Cards is expected to report margin expansion on the back of APR hikes and lower funding costs.

Fresh stress flow easing in Cards, but remains elevated for MFI

MFI stress flow is expected to stay high in Q1FY26, driven by seasonal weakness and the impact of recent ordinances in Karnataka and Tamil Nadu. This will result in elevated LLP for NBFC-MFIs and banks with significant MFI exposure. While PL stress flow has likely peaked, it may remain elevated in the near term. Credit card stress is easing, but issuers are likely to step up charge-offs, which will keep LLP levels high. Corporate asset quality remains stable, so we do not foresee significant NPA formation for PSBs. However, agri/KCC slippages could stay high for some large private and public sector banks due to seasonal trends, warranting higher provisioning. Overall, LLP is expected to moderate but remain elevated in Q1FY26, primarily due to higher charge-offs in unsecured and KCC loan segments.

Prefer banks/NBFCs with earning resiliency amid growth/margin pangs in H1FY26

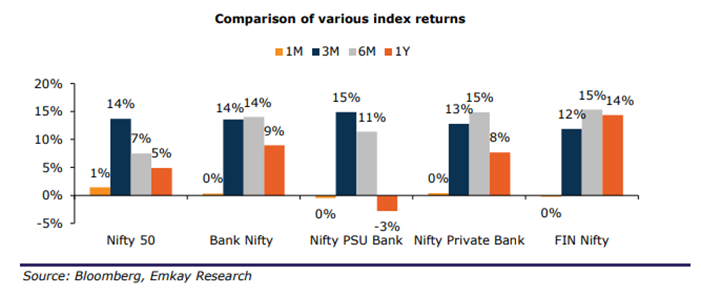

Over the past three months, Bank Nifty has largely mirrored the broader market performance (see Exhibit 7), supported by expectations of improved credit growth driven by monetary and regulatory easing, a peak in unsecured loan stress, and attractive relative valuations. While Emkay expects credit growth to remain subdued in H1FY26 due to weak demand and banks prioritizing margin protection, a recovery is likely in H2FY26, led primarily by secured lending. Although stress in unsecured loans appears to have peaked, we anticipate that NPA formation and LLP will stay elevated through H1FY26 before easing thereafter.

In this context, we prefer banks and NBFCs that demonstrate strong growth, resilient margins, and stable asset quality, positioning them well to benefit from the eventual recovery. Emkay’s top picks include HDFCB, ICICIB, SBI, RBL, KVB, Ujjivan, Indian Bank, and SBI Cards. Among these, Ujjivan and RBL stand out as compelling plays on the asset quality turnaround expected in H2FY26. Ujjivan also holds strong potential to secure a Universal Banking license, along with AU SFB. Accordingly, we have raised our target prices for Ujjivan, RBL, and AU SFB by 18–20%.

Credit card (CIF) continues to fall, while spends pick up

Credit card growth (CIF) slowed to 9% YoY, primarily due to a decline in new card issuances amid rising asset quality concerns, particularly in the sub-Rs 50,000 segment. However, spend growth picked up slightly to 15% YoY in May 2025, aided by seasonal tailwinds. HDFC Bank saw a marginal increase in its CIF market share to 21.8%, while ICICI (16.4%), Axis (13.5%), and RBL (4.3%) experienced slight declines. RBL’s dip reflects a strategic shift toward organic growth following the conclusion of its partnership with Bajaj Finance. Market shares for SBI and Kotak Mahindra Bank remained stable.

Channel checks suggest that fresh stress flows are easing, but issuers are expected to step up charge-offs, leading to higher LLP. We believe the current slowdown—driven by asset quality concerns—is temporary, with industry growth likely to rebound by Q2FY26.

Swift rate-cut cycle to hurt margins for banks

The newly appointed Governor has taken an aggressive stance on monetary easing, slashing the repo rate by 100bps to 5.5% and announcing an additional 100bps cut in the CRR to a historic low of 3%, effective from September to November, in an effort to stimulate growth. Despite these measures, Emkay believes credit growth will take time to gain momentum. Meanwhile, bank margins are expected to compress significantly in H1, driven by the impact of lower repo rates on floating-rate loans. This will be partially offset by banks reducing savings account rates.

The benefits of the CRR cut—and the resulting liquidity infusion—are likely to materialize more meaningfully in H2, offering some relief to margins. For Emkay’s coverage universe, the company anticipates QoQ margin compression in the range of ~5–20bps, with larger private banks at the higher end of the range

and public sector banks at the lower end. Banks such as IDFC First Bank, City Union Bank, SBI, and those with high MFI exposure are expected to see relatively limited margin pressure, while SBI Cards is likely to report margin expansion.